U.S. Bank

Driving Customer Engagement Through Rewards

The Challenge

The Deposit Monetization team at U.S. Bank focused on using rewards to deepen customer relationships and drive loyalty. For Zafin, this meant attracting external cash transfers by offering competitive APYs for qualifying deposits. For multi-product offers, it involved encouraging customers to open and maintain additional accounts by tying cash rewards to specific behaviors. However, limited financial incentives and strict compliance requirements posed significant design challenges. Research was critical to uncovering customer motivations and crafting experiences that balanced business goals with user needs.

The Solution

For Zafin, we designed an interactive calculator to highlight potential rewards, optimized entry points for discoverability, and refined visual hierarchy to make compliance-heavy content more approachable. For multi-product offers, we introduced a gamified status tracker to encourage sustained engagement, ensured accessibility, and streamlined usability.These solutions leveraged creative design to inspire action, turning constraints into opportunities to build trust and drive customer loyalty.

To understand why U.S. Bank features often miss their mark, it’s critical to grasp how internal processes skew the perception of who their customers are. The design org had a layer of bureaucracy who weren’t tied to specific product teams, but rather seemed to spend their time perpetually re-engineering processes, brand guidelines, and assets. It was this team that created what seemed on it’s surface an extensive library of user personas; however, on closer inspection, their lack of engagement in product work hampered their ability to accurately represent our account holders.

The personas were aspirational rather than representative - in fact the overwhelmingly most-cited persona - Maria, the late-twenty-something, six-figure-earning Minneapolis tech worker -is suspicially similar to about 70% 0f the design org itself. I’ve outlined the contrasts between the user that U.S. Bank wants vs. the customers we actually have. The latter is based on official former research documents, conversations I had with dedicated research partners, and my own customer interviews throughout my tenure with U.S. Bank.

Assumption

Prefers digital touchpoints; uses latest devices.

Highly engaged; actively seeks out and researches new products and services to grow their money

Urban, cosmopolitan professionals

Diverse with an even spread among age groups

Reality

Prefers in-person banking; easily fatigued with tech.

Low-information, passive account holders. For example, common common motivations included convenience or legacy reasons—such as proximity to a local branch after moving to a new town or accounts opened by parents during childhood.

Suburban (outside of Minneapolis)

While there is some diversity, demographics skew 35+, white, and female.

By grounding designs in reality rather than aspiration, we increased clarity, usability, and engagement—ultimately delivering products that better served U.S. Bank’s real customers. This deeper understanding of the actual customer base led to critical design decisions:

Zafin Feature: Knowing that most users weren’t financially proactive, introducing a calculator tool will simplify APY comparisons. We can also introduce better visual hierarchy to help passive users quickly grasp the benefits.

Multi-Product Offer: Since users wouldn’t naturally track multiple offers or understand complex steps, adding a visual status tracker with gamified progress indicators will lend clarity, transparency, and accessibility for traditionally tech-adverse users.

Zafin

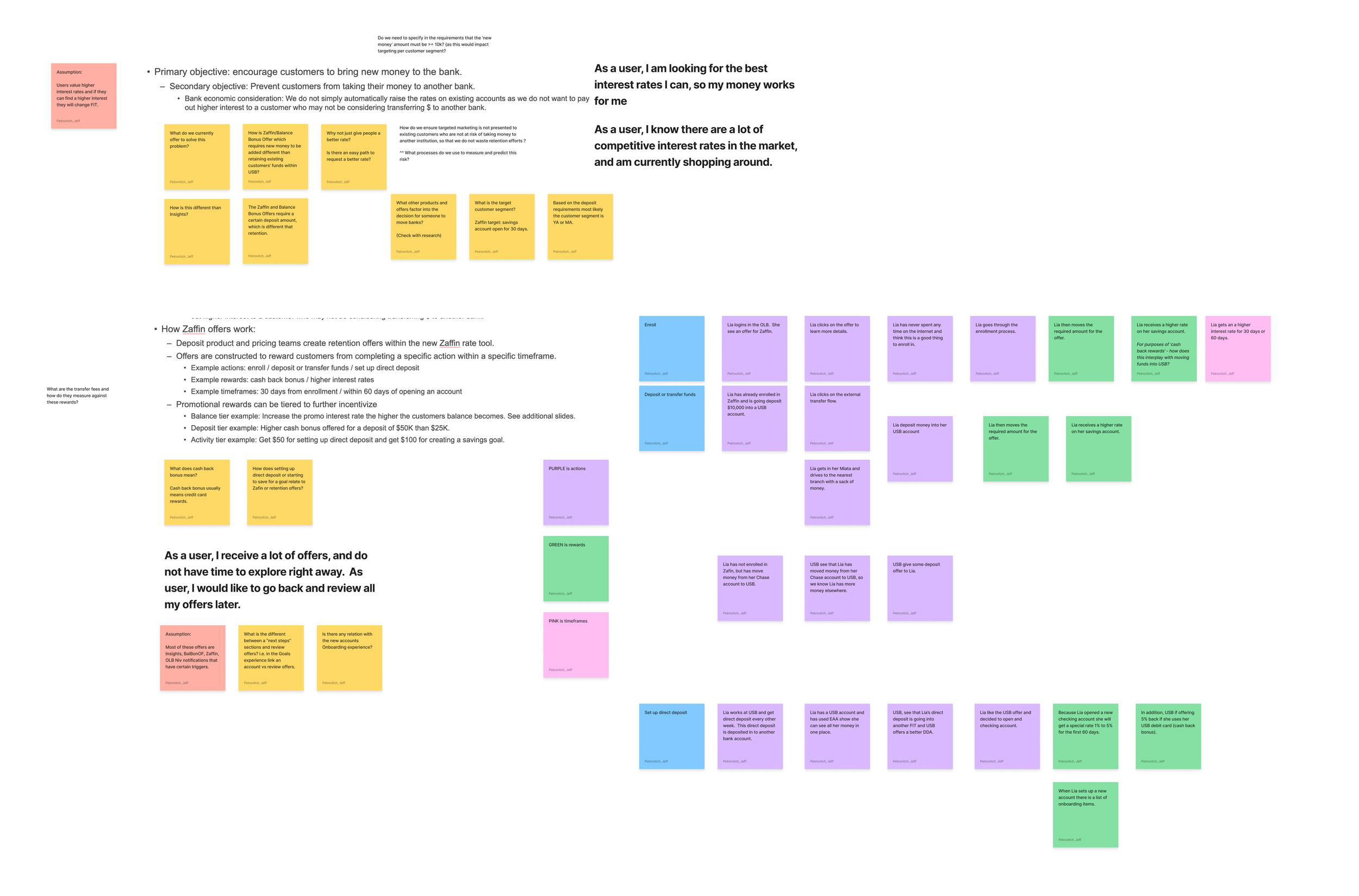

Problem Statement

For this feature’s second iteration, the objective was to improve user engagement by addressing key issues from the initial rollout. Customers with a savings or MMA account open for 30+ days needed a clear pathway to deposit $10K+ through internal/external methods and be made aware of APY increase opportunities. The goal was to reduce account churn and drive new deposits.

Initial Mockups & Findings

The first iteration featured detailed copy, but user testing revealed critical flaws:

Skepticism: Participants viewed the offer pessimistically, searching for disqualifying details in the terms.

Over-reliance on Text: Text-heavy explanations weren’t retained well, even when read aloud.

Preference for Visual Structure: Users preferred structured visuals—tables and graphics were much easier to understand and recall.

Mock-ups from initial round of design

Design Goals

Reduce Skepticism: Introduce structured, visual APY rate tables to clarify potential earnings by deposit type/amount. This approach aimed to enhance trust and make offer details transparent at a glance.

Enhance Comprehension through Interactivity: Add an interactive calculator to allow users to input potential deposit amounts and immediately see their potential earnings. This would make abstract APY rates tangible, increasing user engagement

Use Visual Hierarchy: Find opportunities to present key offer details graphically—using icons, bold text, and bullet points to improve retention of essential information.

Designing solutions for the Zafin feature required balancing user trust, clarity, and compliance-mandated content. Based on user feedback, we focused on creating transparency and improving usability through structured visuals and interactions. Below are the key solutions developed:

Key Solutions

Click an image to enlarge it.

Interactive Calculator

Allowed users to input deposit amounts and transfer types to instantly calculate potential APY earnings.

Built trust by making financial benefits tangible and intuitive to explore.

Tested positively for transparency and ease of use.

APY Rate Tables

Organized APY information into clear, scannable tables categorized by transfer type (external, internal, or no transfer).

Helped reduce user skepticism by presenting information graphically rather than in dense text blocks.

Content Architecture Reorganization and Visual Emphasis and Appeal

Enhanced scannability by prioritizing key details with bold text treatments and reorganized layouts.

Simplified compliance-heavy terms into bullet points or expandable sections, reducing cognitive load while maintaining legal clarity.

Component Library

As the Visual Interaction Designer, I spearheaded the creation of reusable components and interactions for the Zafin feature, including:

Developing the calculator widget and APY tables as scalable, reusable components.

Ensuring accessibility through proper contrast ratios, interactive states, and clear information hierarchy.

Leading efforts to integrate these new components into the official U.S. Bank design library.

Coaching my team on effective Figma file organization and component usage.

We conducted two rounds of moderated usability testing using a clickable prototype, facilitated by a dedicated UX research resource. The goal was to evaluate whether the redesigned feature met business and design objectives while ensuring users could engage with the offer clearly and confidently.

Test Setup

Participants: 6 users (aged 35-55) with varying levels of financial literacy, selected to reflect real U.S. Bank customers.

Testing Format: Remote, moderated sessions lasting 45 minutes each. Users interacted with the prototype and completed key tasks, such as calculating their potential earnings, understanding APY rates, and enrolling in the offer.

Primary Goals:

Assess user comprehension of the offer and APY benefits.

Measure engagement with the interactive calculator and graphical elements.

Identify remaining confusion or skepticism about offer terms.

Key Metrics & Insights

Task Completion Rate:

100% of participants successfully completed the primary task (calculating potential APY using the interactive tool).

83% correctly identified the total APY rate they would earn based on their deposit and transfer type.

Time on Task:

Average time to complete the APY calculation: 2.5 minutes, indicating that users found the feature intuitive.

User Satisfaction:

4.2/5 average rating for ease of use.

67% of participants appreciated the visual organization of the APY rate tables and compliance-mandated terms, but noted that terms were still somewhat dense.

Despite clearer communication, 5 out of 6 users remained skeptical about the offer itself.

Comprehension of Terms:

67% of participants felt confident they understood the offer terms after using the redesigned page.

The inclusion of emphasized rate graphics and bold text treatments improved readability of critical details.

Participants preferred the APY rate tables over long-form text for quickly comparing potential earnings.

5. Qualitative Feedback

Positive:

“The rate table was clear—I could instantly see what I would earn without reading everything.”

“Highlighting the APY percentages in bold helped me decide faster.”

Negative:

“Even though I understood the offer better, it still didn’t seem worth it unless I was moving a large amount.”

“I liked how the terms were broken down, but I still felt like there might be a catch somewhere.”

Multi-Product Offers

Problem Statement

U.S. Bank’s existing customers often maintain only a limited relationship with the bank, holding just one or two product types. The business goal was to encourage these customers to deepen their engagement by opening new checking or savings accounts, with cash incentives as motivation. Customers needed a clear way to track progress toward meeting the requirements for earning rewards. Our objective was to design a streamlined, transparent experience that would support this initiative by increasing account volume, deposits, and product stickiness.

Context

This was U.S. Bank’s first attempt at building a product offer-tracking feature, and it came with unique challenges. Unlike projects with established requirements or prior feedback, we were given vague guidance. This lack of clarity stemmed from a cultural tendency to avoid accountability—product teams intentionally kept the requirements broad, creating ambiguity around success criteria. As a result, much of our effort went into refining the product vision and translating abstract goals into actionable design elements.

To avoid overwhelming the reader with every intricate detail of this refinement process, we’ve included key artifacts, such as brainstorming documents, competitive analyses, and use case mapping, to illustrate how we tackled the complexity. Our research and ideation helped fill the gaps left by unclear requirements, ensuring the final solution met both user and business needs.

Design Goals

Clarify Complex Offer Requirements

Translate vague and multi-step offer requirements into a straightforward user experience that clearly communicates eligibility criteria, necessary actions, and reward outcomes.Build Trust with Clear Progress Tracking

Create a transparent progress-tracking mechanism that gives users real-time feedback on their journey toward earning rewards.Encourage Full Engagement

Provide incentives and reminders to motivate customers to complete all required steps and open both a Smartly Checking and Standard Savings account.Use Visual Elements to Simplify Complex Information

Incorporate rate tables, visual indicators, and clear text treatments to break down the dense terms and conditions into digestible components.

Key Solutions

Click an image to enlarge it.

Progress Tracker

Enabled users to track their progress toward multiple rewards, each with required steps.

Included clear indicators for task status (completed, in progress, or time-sensitive).

Accessible Status Icon Design

Collaborated with accessibility partners to redesign status indicators with paired text descriptions.

Ensured all users, including those with visual impairments, could confidently follow their progress.

Gamified Reward States

Highlighted completed tasks with visually engaging banners.

Used neutral tones (orange instead of red) to indicate incomplete steps, maintaining a positive experience.

Opt-In Ads for Missed Rewards

Designed ads encouraging users to re-engage after missing a reward or opting out.

Emphasized opportunity over failure to keep the experience positive and motivating.

Once the multi-product offer design was finalized, we conducted two rounds of moderated usability testing using a high-fidelity clickable prototype. Six participants matching the target demographic—existing U.S. Bank customers with certain products but lacking checking and/or savings accounts—were recruited. The research was structured to assess:

Progress Tracker Usability: Did users intuitively understand how to track their progress toward earning rewards across multiple offers and steps?

Clarity of Status Indicators: Were users able to distinguish between completed steps, pending actions, and time sensitivity effectively?

Effort Perception: How did users perceive the overall effort required to earn the rewards?

Results Summary

Progress Tracker Feedback

80% of participants correctly tracked their progress across multiple offers.

Participants appreciated the clear step-by-step breakdown, but two users mentioned that the amount of information would feel overwhelming if there were more than two offers being tracked at a time.

Status Indicators Effectiveness

85% of users found the color-coded indicators helpful in identifying completed and pending tasks.

Time-sensitive indicators were noted as clear, though users requested more prominent warnings when nearing the expiration date of an offer.

Effort Perception

Several participants expressed concerns about the number of steps required to earn rewards, noting that while the visual design made the process clear, the effort felt excessive. One participant remarked, “This feels like too much work for what I’m getting in return.”

Two users specifically suggested that breaking larger tasks into smaller milestones with mini-rewards might improve motivation.

4. Key Qualitative Feedback

“I like that I can see exactly what’s left to do, but it would help if the steps were grouped better.”

“The countdown timer is helpful, but maybe show how much time I have left right on the tracker instead of only in the details.”

“It’s nice that everything’s clear, but it feels like a lot of effort for a simple reward.”

Iteration and Conclusion

Both features in this case study—Zafin and Multi-Product Offers—highlight the iterative process of addressing unique customer needs while navigating restrictions. For Zafin, the challenge was building trust and engagement in a scenario where financial offers lacked clarity and appeal. We introduced interactivity, refined messaging, and improved content hierarchy to create a transparent and user-friendly experience. For Multi-Product Offers, the focus shifted to motivating users through gamification and progress tracking, balancing accessibility and compliance while driving deeper account relationships.

Together, these projects exemplify the Deposit Monetization team’s ethos: enhancing customer engagement and loyalty by meeting users where they are. By iterating on research insights, cross-functional collaboration, and design precision, we delivered solutions that addressed business goals while fostering user trust and clarity—making incremental yet impactful strides in strengthening customer connections.